What a difference a year can make.

Most participants remember what their retirement portfolios looked like a year ago, and few would likely want to return to that place.

A year later though, most TSP funds have recovered and beat last year’s returns before the insanity started.

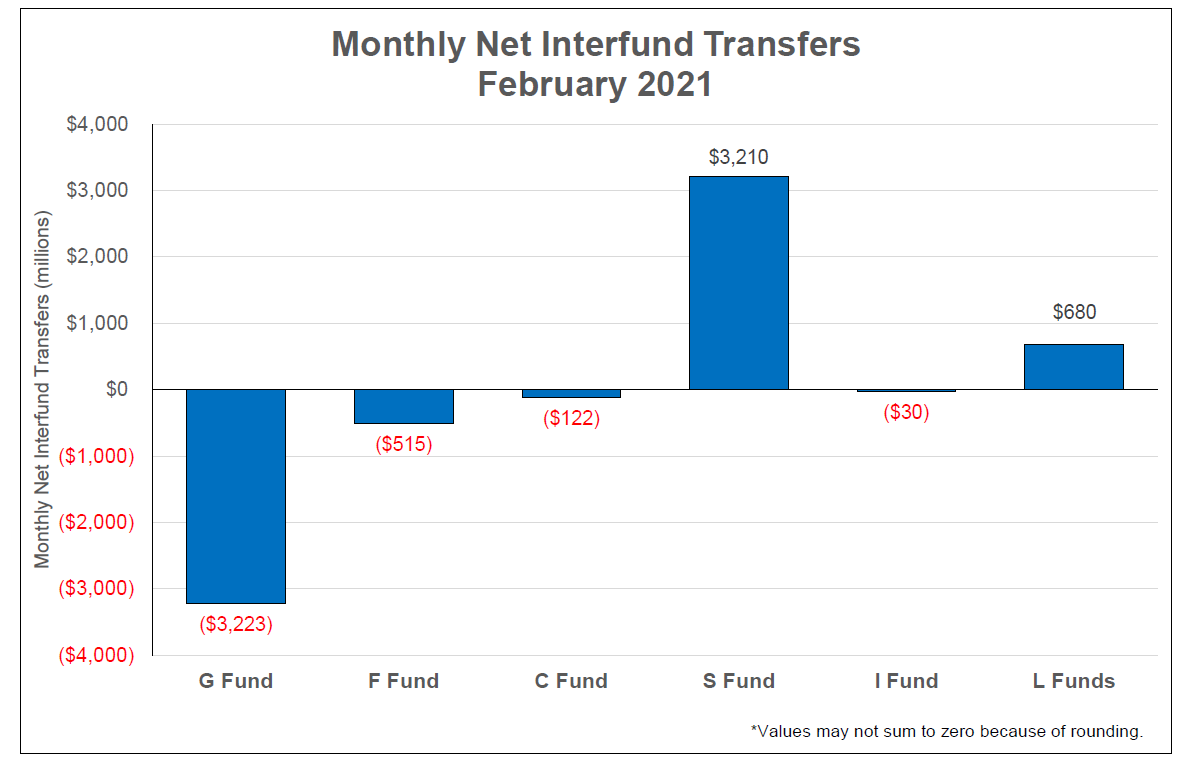

Fearing the volatility, TSP participants rolled $9.2 billion into the G fund last February. During the last six days of February and first half of March, participants transferred $21 billion into the G fund.

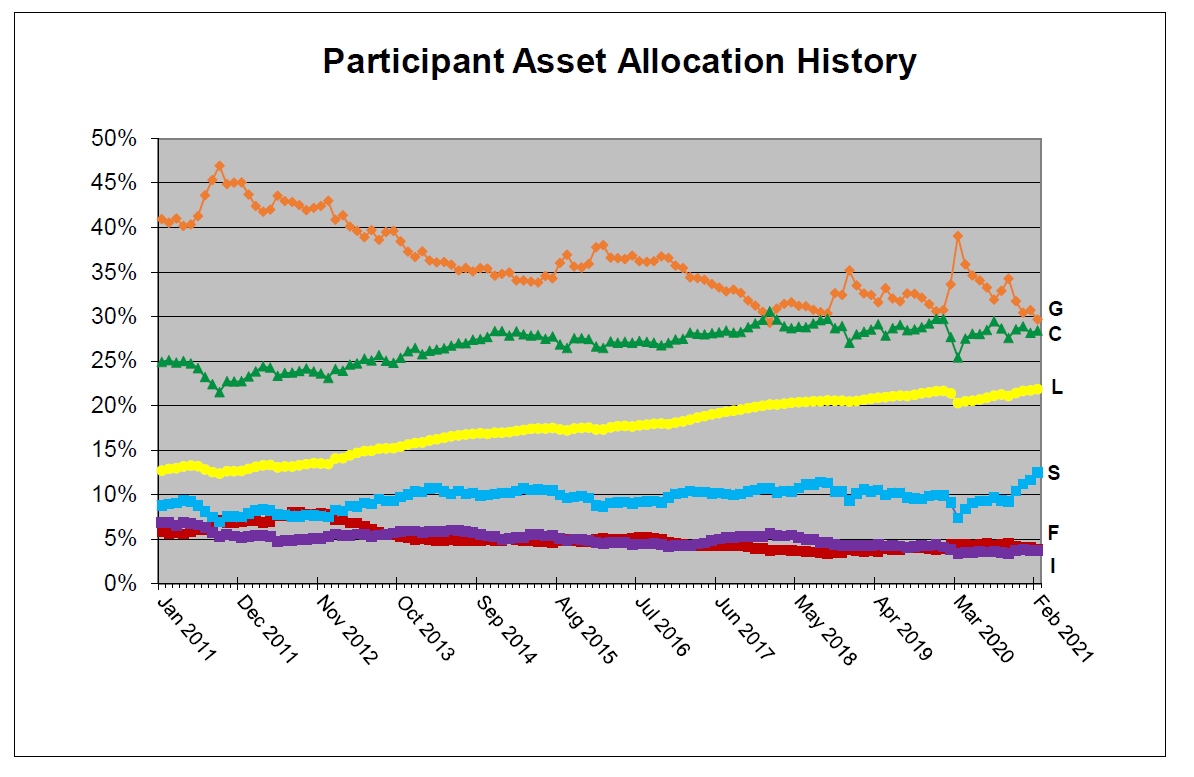

About a year later, the picture looks a little different. The G fund, which is invested in special Treasury funds, is still popular, but participants are noticing decent returns from other the TSP’s other options too.

Participants rolled roughly $3.2 billion out of the G fund in February and into the S and L funds. Money left the F, C and I funds last month as well, though those transfers were much smaller.

Inter-fund transfers are the exception, not the norm for most TSP participants, Sean McCaffrey, the Federal Retirement Thrift Investment Board’s chief investment officer, said last Monday at a monthly board meeting.

A relatively small number, or just 5% of TSP participants, were responsible for the large volume of inter-fund transfers last spring.

Still, it’s one indication of how participants are feeling about the stock market, as some participants flee to the usually-safe G fund when things get rocky. You can see evidence of that here.

This all comes as the rates of return for the G fund continue to decline, as they have been for the last 30 years or so.

The year-to-date return for the G fund over the last 12 months sits at 0.82%. For January and February it sits at 0.15%.

It’s a stretch to say participants are over the G fund, — just under 30% of TSP assets are invested in it — but other TSP funds are picking up popularity.

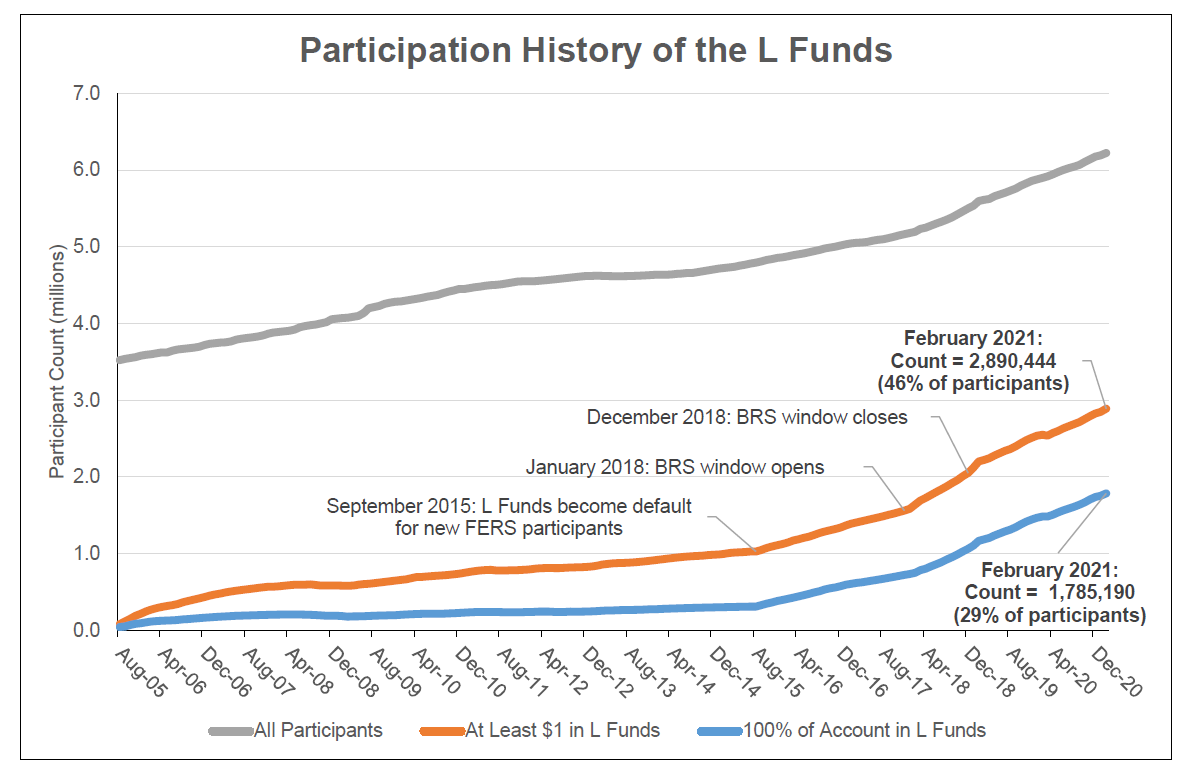

The L funds have done well in recent months, especially after the TSP added additional lifecycle options last year.

The TSP created the L funds back in 2005. The goal was to create a series of funds that allows participants to better target their investments toward their own goals and timelines, adjusting risk downward as they approach retirement. The new five-year lifecycle increments give participants the option of further targeting their investments to an even more specific retirement date.

As of February, 46% of all TSP participants have invested at least some of their savings in one of the L funds. About 29% of participants have their entire TSP accounts invested in one of the lifecycle options.

The TSP board attributes the rise, in part, to the influx of new military members who have joined the plan through the blended retirement system.

The new L funds help too, though the most popular options remain the 2030, 2040 and 2050 funds, according to TSP data. The L2030 has the most assets, but the L2050 has the most participants, about 1.4 million people.

What else helps? A reminder or two. The TSP sent annual statements to its participants in recent weeks, which also could have prompted some to think about how their assets are allocated.

“It’s not uncommon for those statements inspire participants to take a fresh look at their TSP accounts,” McCaffrey said.

Nearly Useless Factoid

By Alazar Moges

Mickey Mouse is one of the most beloved and recognizable characters. But Walt Disney originally named the first iteration of the iconic character Mortimer Mouse. At the urging of his wife Lillian, who disliked the name, he changed it to Mickey.

Source: Library of Congress

Comments are closed.